On February 26, 2025, the European Commission presented the so-called “Omnibus I Package” with the aim of simplifying the existing sustainability reporting rules and related obligations. This package includes adjustments to the Corporate Sustainability Reporting Directive (CSRD), the EU Taxonomy Regulation, and the Corporate Sustainability Due Diligence Directive (CSDDD). The proposed changes are intended to reduce the administrative burden on companies and strengthen their competitiveness without jeopardizing the EU's sustainability goals.

Background to the Omnibus Initiative

In recent years, the European Union has introduced a series of directives and regulations to require companies to report on their sustainability practices and ensure that their supply chains comply with human rights and environmental standards. However, these measures were perceived by many companies as bureaucratic and costly, leading to calls for simplifications. The Omnibus I package is the EU Commission's response to these concerns.

The main proposed amendments

Overview of the regulatory changes to CSRD, EU Taxonomy, and CSDDD

All important Omnibus proposals in detail

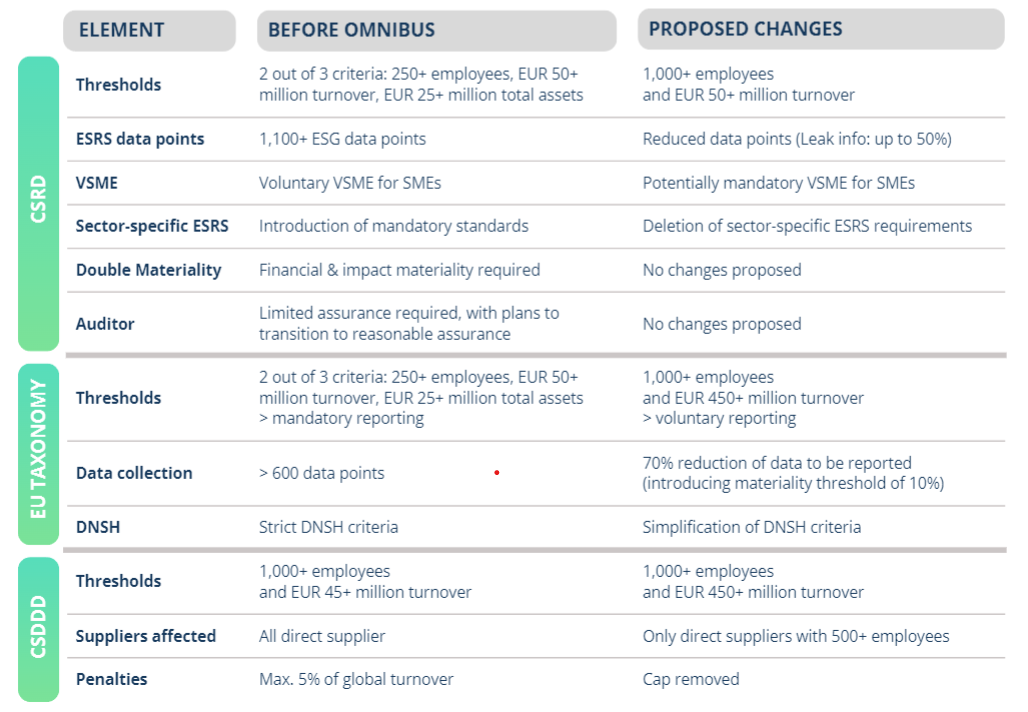

Corporate Sustainability Reporting Directive (CSRD)

- Scope of application: The thresholds for large companies subject to reporting requirements have been raised. The proposal stipulates that, initially, large companies with more than 1,000 employees will be subject to the reporting requirement. The criteria for large companies' sales revenue (€50 million) and balance sheet total (€25 million), on the other hand, are to remain unchanged. Instead of the 2-out-of-3 criteria selection, those who reach the new number of employees and either the turnover or the balance sheet total are considered to be subject to reporting. The new provisions apply analogously to parent companies of large groups. This relief also includes some companies from the first CSRD wave that were already subject to reporting for the 2024 financial year. These changes reduce the number of reporting companies by about 80%.

- Revision of ESRS data points: The European Sustainability Reporting Standards (ESRS) are to be updated and simplified to reduce the number of required data points (estimates suggest a reduction of up to 50%), clarify unclear terms, and improve consistency with related EU initiatives.

- Adjustment of the value chain cap: Companies required to report may only request information from non-reporting companies in their value chain if these companies are included in a voluntarily applicable sustainability standard. Exceptions apply only to specific requirements relevant to certain industries. Previously, this request function was assigned to the more comprehensive LSME ESRS (for capital-market-oriented SMEs). This new regulation is intended to reduce the so-called trickle-down effect.

- Sector-specific ESRS and LSME: The introduction of sector-specific standards and LSME ESRS is no longer planned.

- VSME: A voluntary standard for SMEs (VSME) is to be adopted by means of a delegated act.

- Audit of reports: The legal requirement for an audit remains in place. However, the transition to reasonable assurance is no longer applicable. This is because the audit of the sustainability report is only to be carried out with limited assurance in the long term. A future increase in the level of assurance to reasonable assurance and the development of corresponding audit standards are no longer planned.

EU Taxonomy Regulation

- Adjustment of scope: The EU Taxonomy will only apply to companies required to report under the CSRD that have a turnover of more than €450 million; for other reporting companies with a turnover of less than €450 million, the reporting requirements of the Taxonomy Regulation are to be handled in a more “flexible” way. The exact proposals for this are still pending. A separate Omnibus proposal for the EU Taxonomy is expected in the coming months.

- Simplification of reporting requirements: A 10% materiality threshold for economic activities will be introduced and there will be a tiered materiality concept for individual KPIs. Less important KPIs can be omitted under certain conditions. At the same time, the previously strict DNSH criteria and the OpEx disclosures are to be simplified. In addition, around 70% of the reportable data points are to be eliminated by simplifying the reporting templates.

- Reporting templates: The reporting templates for the EU Taxonomy are to be simplified.

- Voluntary taxonomy reporting: Companies that are not required to report on taxonomy but are covered by the CSRD can report voluntarily. If they do so, they must disclose their turnover and investment figures and can decide whether to disclose their operating cost figures.

Corporate Sustainability Due Diligence Directive (CSDDD)

- Simplifications to due diligence: A company's due diligence is now limited to direct suppliers (direct business partners; Tier 1) with more than 500 employees. Companies are exempt from assessing the impact on indirect partners unless information is available about potential negative impacts. In addition, the obligation to terminate business relationships as a last resort has been dropped; instead, they should be suspended. The cycle for assessing business relationships and the effectiveness of due diligence measures has been extended from one year to five years.

- Definition of measures: Companies are still required to develop a transition plan to mitigate climate change, which includes specific measures to achieve their targets. However, there is no longer an explicit obligation to implement these measures.

- Company-specific assessment: The company-specific due diligence review is now due every five years instead of the annual review that was previously planned.

- Civil liability: The EU-wide civil liability regime has been dropped, and the obligation of Member States to allow victims to be represented in court by civil society organizations has been removed. Companies are, therefore, subject to the applicable liability regimes of the Member States.

- Penalties: periodic penalty payments now no longer amount to at least 5% of the obligated company's worldwide net turnover in the financial year. The cap has been removed. The scale of fines imposed has been reduced, so even minor offenses should lead to fines.

The new timeline of CSRD, EU Taxonomy, and CSDDD

New CSRD timeline according to the Omnibus proposal

- January 1, 2025:

- Companies already affected by the CSRD reporting requirement before 2025 and still fall under the new proposed CSRD scope must, as initially intended, report for the 2025 financial year but only fulfill the proposed reduced reporting requirements.

- According to the proposals, companies in the first CSRD wave that still have to be exempted, i.e., large public-interest entities with a workforce of 501 to 1,000, are not covered by the proposed postponements (derivation of the ASCG from Article 1 and 2 Amendment Directive #2 in combination with Article 5 of Amendment Directive #1).

- Companies already affected by the CSRD reporting requirement before 2025 and still fall under the new proposed CSRD scope must, as initially intended, report for the 2025 financial year but only fulfill the proposed reduced reporting requirements.

- January 1, 2027: Start of CSRD reporting for large companies that have so far been and will continue to be required to report for the 2025 financial year.

- January 1, 2028: Start of CSRD reporting for large companies that have not yet been required to report.

- January 1, 2029: Start of reporting requirement for listed small and medium-sized enterprises (SMEs), small credit institutions, and captive insurance companies.

New EU Taxonomy timeline according to the Omnibus proposal

- Current financial year 2025: The amendments to the EU Taxonomy are to apply to the current financial year 2025, i.e., to reporting from January 1, 2026. Detailed information is expected with the publication of a separate EU Taxonomy Omnibus proposal.

New CSDDD timeline according to the Omnibus proposal

- July 26, 2027: Extended deadline for transposing the CSDDD into national law.

- January 1, 2029: Introduction of the first CSDDD due diligence requirements for companies with 3,000 employees and €900 million in revenue.

- January 1, 2030: Introduction of due diligence for companies with 1,000 employees and a turnover of €450 million.

The next steps: adoption and entry into force of the timeline

After publication by the European Commission on February 26, 2025, the Omnibus proposal will now be examined by the relevant parliamentary committees and by the member states in the Council. During this process, amendments may still be made, particularly in inter-institutional negotiations (“trilogue”) if different positions exist. During this phase, companies and associations often still have the opportunity to submit comments.

As soon as an agreement has been reached, the final vote takes place:

- The European Parliament decides by majority vote

- The Council of the EU must agree by a qualified majority

After adoption, the law is published in the Official Journal of the European Union and usually enters into force 20 days later. The exact adoption is expected in the course of 2025. The implementation phase for the member states then begins:

- Amending Directive #2 (concerns the temporal changes) must be transposed into national law by the EU member states by December 31, 2025, at the latest.

- Amending Directive #1 (concerns the substantive changes) must be transposed into national law by the EU member states within 12 months of entry into force.

Note: It is expected that EU member states will have to implement the amending directive more quickly than the regular 12-month period so that not only the timing but also the content of the changes are in place by the end of 2025. Therefore, companies should prepare for possible adjustments at an early stage and closely monitor further developments in legislation.

The VSME and the newly proposed small-and-mid-cap category

With the introduction of the Omnibus Initiative and the proposed small-and-mid-cap category, smaller companies, estimated to have 250-1,000 employees, could face new sustainability reporting requirements. Small and mid-cap companies that were not previously required to report may also have to provide sustainability information in the future but in a simplified form. This is where the VSME (Voluntary Sustainability Monitoring and Reporting Standard) comes into play. This voluntary standard could provide a mandatory basis for these companies in the future. However, there are no concrete statements about the VSME as a possible mandatory standard yet; so far, it is only an idea.

VSME was designed as a slimmed-down version of the ESRS (European Sustainability Reporting Standards) to provide smaller companies with a more straightforward way to collect and report relevant sustainability data. If the standard becomes mandatory for the new small- and mid-cap category, these companies could benefit from a clear and structured but less complex solution. The VSME would enable them to efficiently collect the information required of larger, reportable companies while minimizing the effort involved. In this way, the VSME could serve as a bridge to introduce smaller companies to the world of sustainability reporting without overwhelming them with the extensive requirements of the ESRS.

What companies should do now

The Omnibus Initiative brings important changes to sustainability reporting that affect both small and large companies. Find out below what adjustments are needed to meet the new requirements.

Large companies: Adjustments and integration of reporting

For large companies, the Omnibus Initiative requires adjusting reporting systems to the new ESRS requirements. Sustainability and financial reporting must increasingly be integrated. In addition, companies should review their due diligence processes in the supply chain to meet the requirements of the CSDDD.

Small companies: Review of reporting requirements and preparation

Small companies should check whether they are affected by the new relaxed thresholds. Depending on this, a reporting requirement could arise in the future. The final amendments to the ESRS and the proposals for a new small and mid-cap category and any new reporting requirements that may arise from this should be monitored to prepare for the latest requirements in good time.

Critics and concerns about the Omnibus simplifications

The aim of the Omnibus Initiative to reduce red tape for companies is to cut administrative burdens. However, some associations, industries, and companies are already expressing concerns. There are several critical voices, which are summarized below:

- Increased complexity for smaller companies: Despite the intended simplification, introducing new reporting requirements could increase the administrative burden for smaller companies, especially if they have to adapt quickly to the new standards.

- Lack of clarity in the requirements: Some companies fear that the new regulations, particularly the adjustments to the ESRS, are not sufficiently clear and precise. This could lead to uncertainties in their practical implementation.

- Delays in implementation: The uncertainty regarding the final timeframe and the details of the changes is a cause for concern for many companies, as it seems complicated to prepare for the new requirements in good time.

- Less responsibility and carelessness when it comes to sustainability: Environmental and human rights organizations, in particular, fear that the relaxation will lead to a weakening of sustainability reporting and that companies will have fewer incentives to take social and ecological responsibility seriously.

- Lack of sector-specific ESRS standards: Some companies criticize the lack of sector-specific standards, which makes it difficult to compare companies within the same industry. A general standard could lead to industry-specific characteristics not being sufficiently considered.

Envoria and the Omnibus Proposal: Flexibly Prepared for the Future

The EU's Omnibus initiative is bringing about changes. While the new regulatory proposals not only influence companies' ESG reporting, they also change the market for sustainability software – but we at Envoria are well prepared for this. Our all-in-one software for ESG and financial reporting is flexibly structured and prepared for all scenarios – whether for companies that continue to be subject to reporting requirements or for those that are excluded for the time being by the new thresholds but still want to publish their sustainability report.

Thanks to our early preparation and ability to quickly implement regulatory changes, you can be sure that your sustainability reporting will always be up to date. We offer you a solution that not only integrates the ESRS and VSME standards but also offers the option of responding to future adjustments with individual KPIs. This means you are well prepared for the future, regardless of the changes.

Whether your organization is a large corporation or a small business, Envoria ensures you have the right tools for your sustainability reporting. Our software helps you to easily meet both current and future requirements and to future-proof your processes.