Note: Both companies in the construction industry and companies in other industries are affected by the challenges mentioned in this article. If an industrial company commissions the construction of a new building, the company must also evaluate this building according to the criteria presented in this article since it represents an investment.

On July 12, 2020, the EU Taxonomy Regulation entered into force as part of the European Commission's 2018 Action Plan on Sustainable Finance. It aims to direct capital flows towards sustainable investments, limit/avoid greenwashing, increase transparency for non-financial information, and therefore contribute to the main goal of the EU Green Deal – to achieve zero net greenhouse gas emissions in the EU by 2050.

The EU Taxonomy itself is a classification system that provides companies, investors, and policymakers with a clear definition of what should be considered an environmentally sustainable economic activity.

The importance of the building and construction sector to achieve climate targets

The building sector plays a crucial role when it comes to achieving climate neutrality. According to the European Public Real Estate Association (EPRA), the building sector is responsible for 40% of energy consumption and 36% of greenhouse gas emissions in the EU. In order to achieve the Paris Agreement Goals, the Global Alliance for Buildings and Construction even states that the average building energy intensity per square meter must decrease by at least 30% by 2031.

These figures illustrate the great efforts for change that need to be made in the real estate and construction sector. This applies not only to new constructions but also to existing buildings.

The EU Taxonomy for sustainable activities and to which companies it applies

An economic activity can be considered environmentally sustainable if it can be associated with a taxonomy activity,complies with the Technical Screening Criteria (TSC) to make a significant contribution to at least one of the six environmental objectives and does not significantly harm (DNSH) any of the remaining environmental objectives, and meets the minimum safeguards based on certain global human rights standards and frameworks.

Not sure how to identify your business activities? Find out in our Insight article.

The Technical Screening and DNSH criteria are set out in so-called delegated acts, which supplement the EU Taxonomy. Currently, these legal acts only exist for two of the six environmental objectives, climate change mitigation and climate change adaption. Recommendations for legislation have already been submitted to the EU Commission for the four remaining environmental objectives. However, the subsequent consultation and legislative process is expected to last until 2023. The recently published FAQ documents made clear that there is no application of those objectives before 2024.

Companies in scope of the CSR are already required to report on activities contributing to the first two environmental objectives of the EU Taxonomy. Reporting on all six objectives will start in 2024. Large companies that meet certain criteria need to disclose their activities on the EU Taxonomy from 2025 onwards as the EU Taxonomy is linked to the CSRD.

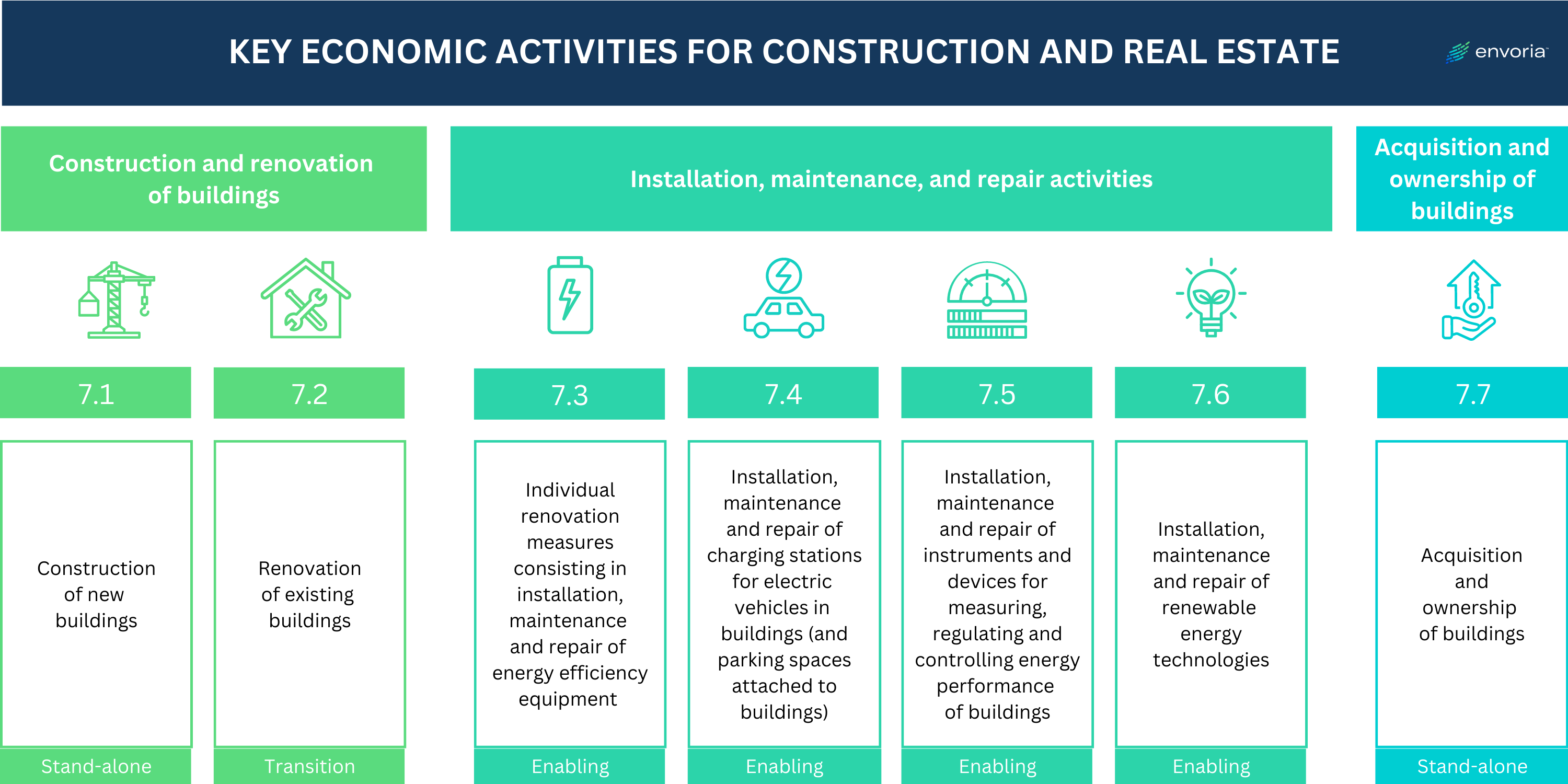

Which are the key EU Taxonomy economic activities for construction and real estate?

Construction and real estate operations are bundled in Section 7 of the Technical Screening Criteria document of the European Commission (p.166), which includes seven activities:

Construction of new buildings

Renovation of existing buildings

Installation, maintenance, and repair of energy-efficiency equipment

Installation, maintenance, and repair of charging stations for electric vehicles in buildings (and parking spaces attached to buildings)

Installation, maintenance, and repair of instruments and devices for measuring, regulating, and controlling the energy performance of buildings

Installation, maintenance, and repair of renewable energy technologies

Acquisition and ownership of buildings

In general, the EU Taxonomy is a binary approach, meaning that economic activities are either compliant with the regulation or they are not. However, “transition” and “enabling” activities have also been included in the regulation. Therefore, the EU Taxonomy does not only include activities that are already green (“stand-alone”), but also activities that are on a transition pathway and activities that directly enable other activities to make a substantial contribution to an environmental objective, such as essential parts of the supply chain. The definition of those types of activities is predefined by the commission and not subject to own interpretations.

The challenge to meet Technical Screening and DNSH criteria for economic activities

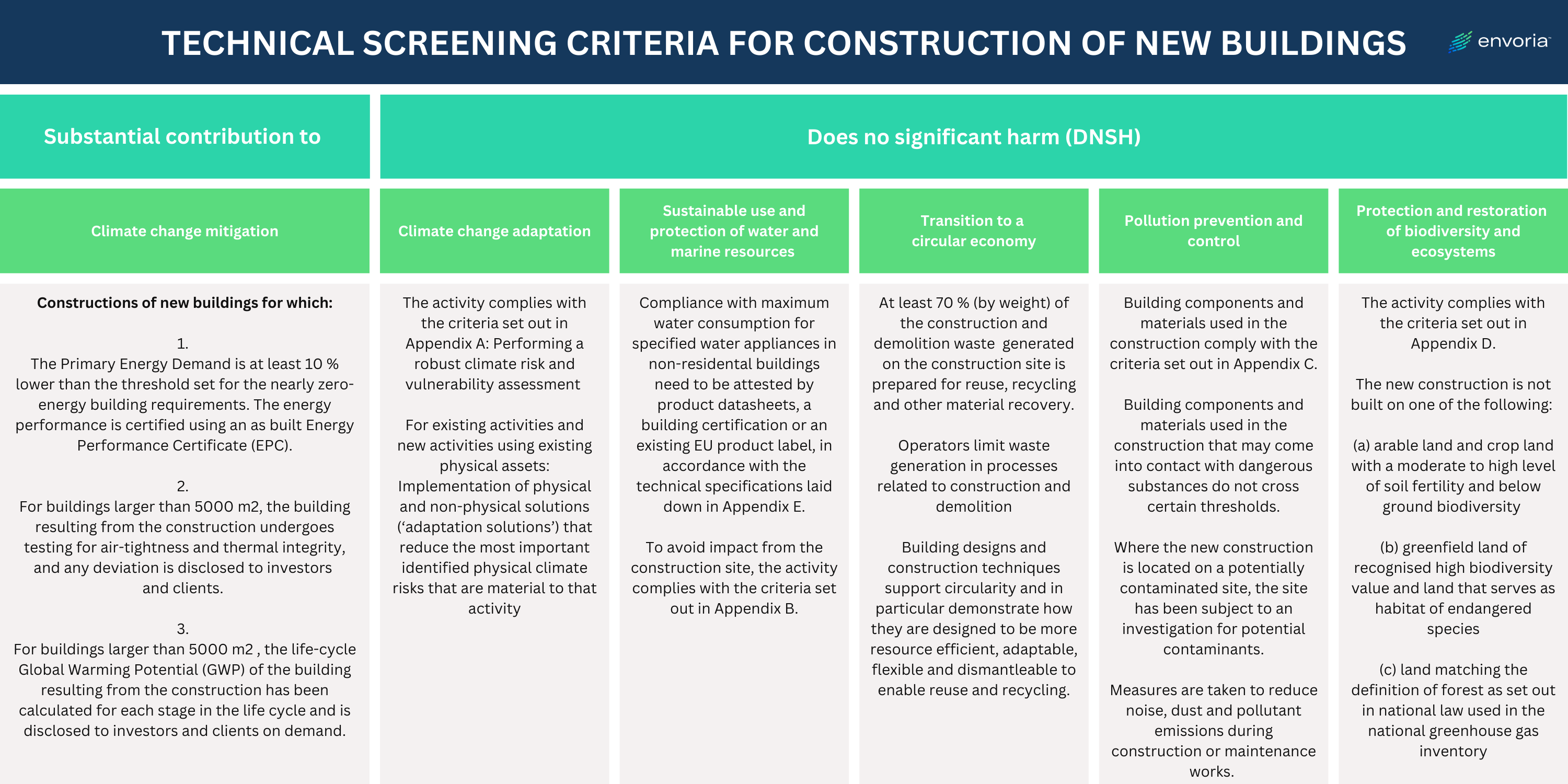

Looking at the Technical Screening Criteria and, in particular, at the DNSH criteria for the exemplary environmental objective of climate change mitigation in the construction and real estate sector, it becomes clear which extensive data is necessary to determine an economic activity as environmentally sustainable. See the example in the graphic below.

The required information to report goes beyond the data currently available. While basic information can be easier determined, it gets more difficult to prove that an activity does not do any harm to the other five objectives.

For example, the energy quality of a building can be determined and verified through Energy Performance Certificates (EPC). However, while planning the construction of a new building, physical climate risks such as floods or hurricanes are usually studied based on past data. But often, there is no analysis of individual physical climate risks for up to 30 years, as required by the EU taxonomy. The requirement to integrate and implement adaptation solutions also goes beyond current building code requirements. This dilemma affects only one of five other objectives that must not be harmed. This makes reporting on the EU Taxonomy a real challenge for all companies operating in the real estate and construction industry.

In addition, the regulation itself does still raise many unclear interpretations within the definition of business activities and its differentiation. However, we see that a lot of property developers try to align their work with the EU taxonomy for future projects.

What to expect in the future

In summary, the construction and real estate industry is facing major challenges due to the disclosure requirements of the EU Taxonomy Regulation. Among the biggest challenges are the complexity and a large number of criteria. Regarding the data required for verifying and reporting environmentally sustainable economic activities, there is still a lack of structured data collection processes and databases with access for companies.

However, further development of the current status of the EU Taxonomy can be expected in the upcoming months. This also applies to the construction and real estate sectors precisely because of their high environmental impact. With the inclusion of EU environmental targets three to six in the Taxonomy Regulation, further regulations and clearer requirements for the industry will be added.

Sustainability reporting in accordance with the EU Taxonomy can be time-consuming and difficult. Envoria's software can help you disclose your economic activities according to the EU Taxonomy. Also, our ESG experts can help you implement your reporting process. Request a free demo to learn more.