The CSR Directive Implementation Act (German: CSR-Richtlinie-Umsetzungsgesetz, CSR-RUG) is a German regulation based on the EU policy 2014/95/EU which requires large companies in Germany to publish non-financial information. The regulation went into effect in 2017, transposing the EU’s Non-Financial Reporting Directive (NFRD) into German national law.

CSR-RUG Timeline

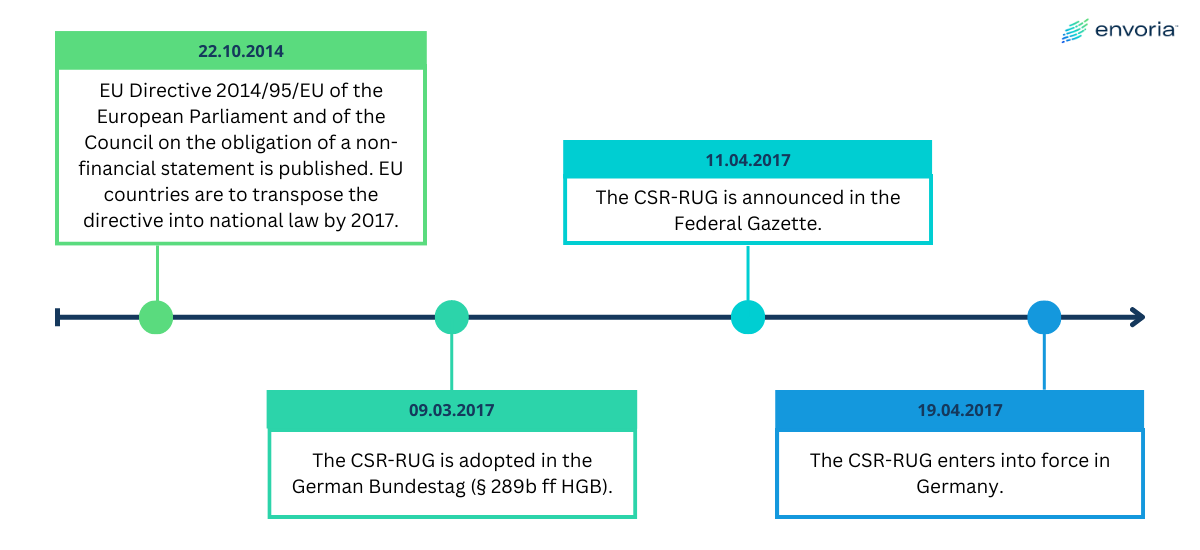

22.10.2014 EU Directive 2014/95/EU of the European Parliament and of the Council on the obligation of a non-financial statement is published. EU countries are to transpose the directive into national law by 2017

09.03.2017 The CSR-RUG is adopted in the German Bundestag (§ 289b ff HGB)

11.04.2017 The CSR-RUG is announced in the Federal Gazette

19.04.2017 The CSR-RUG enters into force in Germany

Which companies are affected by the CSR-RUG?

The CSR-RUG applies to capital market-oriented companies, financial service providers, and insurance companies that meet the following two conditions:

At least 500 employees on an annual average

Balance sheet total of more than EUR 20 million euros or revenue of more than EUR 40 million

What do companies need to report?

With the CSR-RUG, companies need to report their non-financial information, which includes key figures for the following areas:

Environmental aspects

Social aspects

Respect for human rights

Anti-corruption measures

Employee concerns

However, neither the EU Directive nor the German implementation law specifies any concrete content. Within the five aspects, only examples are suggested.

The disclosure obligation calls for an explanation that includes all information necessary to comprehend the business's financial performance, operational results, and overall state. This explanation must also address issues related to the five areas mentioned above.

How do companies need to report?

Organizations are free to choose whether to publish their information as an extension of the management report in the annual report (non-financial statement) or in a separate sustainability report (non-financial report) published no later than four months after the end of the financial year.

The CSR-RUG does not require a specific standard to be used for reporting. Potentially available options for affected companies are the UN Global Compact, EMAS, or ISO 26000. The German Sustainability Code and GRI even cover all requirements of the CSR-RUG reporting obligation.

Significance and prospects of the CSR-RUG

The CSR-RUG represents the German-ratified version of the Non-Financial Reporting Directive, which entered into force in 2018. In April 2021, however, a proposal for a Corporate Sustainability Reporting Directive (CSRD) was published by the EU Commission, which was adopted and came into force on January 5, 2023. This means that the NFRD will be gradually replaced by the CSRD from 2024. Thus, German legislation will also have to adapt to the new European regulations. Compared to the NFRD, the CSRD stipulates stricter disclosure requirements in sustainability aspects for companies. These include, among other things, an expansion of the group of addressees to include companies with more than 250 employees from 2025, the principle of double materiality, and the introduction of uniform EU reporting standards, the European Sustainability Reporting Standards (ESRS).

The CSR-RUG will therefore have to be amended or replaced in accordance with the new EU requirements as a result of the CSRD. Nevertheless, the CSR-RUG represents an important step in German legislation on corporate sustainability reporting, as it forms a basis for future regulations and laws.