In December 2024, EFRAG published the Voluntary Standard for non-listed Micro, Small, and Medium-sized Entities (VSME). Initially, the standard was intended as a leaner alternative to the mandatory ESRS for SMEs. However, with the Omnibus proposal presented on February 26, 2025, the VSME could take on a new, crucial role in ESG reporting.

In this article, you will learn everything about the background, target group, and significance of the VSME standard – before and after the Omnibus proposal.

On February 26, 2025, the European Commission presented the so-called “Omnibus Package” with the aim of simplifying the existing sustainability reporting rules and related obligations. This package includes adjustments to the thresholds, content, and timeline of the EU Taxonomy Regulation. Please note: The Omnibus proposal has not yet been finally adopted – following publication by the European Commission, it is now being examined by the relevant parliamentary committees and by the member states in the Council. During this procedure, amendments may still be made, particularly in inter-institutional negotiations (“trilogue”) if different positions exist. Here, you will find EFRAG's latest version of the VSME from December 2024. Please note that the content may still change due to the omnibus proposal. |

|---|

What is the VSME standard?

The VSME (Voluntary Sustainability Standard for non-listed SMEs) was introduced by the EFRAG in December 2024 as a new voluntary sustainability reporting standard for micro, small, and medium-sized enterprises (SMEs).

At this stage, this standard should serve as a slimmed-down and less complex alternative to the comprehensive European Sustainability Reporting Standards (ESRS). The VSME standard covers similar sustainability topics as the ESRS for large companies. It is intended to provide a more straightforward approach for smaller companies to collect and report relevant sustainability data. It takes into account the fundamental characteristics and needs of micro, small, and medium-sized companies and their limited resources compared to large corporations.

Who is the target group of the VSME standard?

The VSME was initially designed for companies whose securities are not admitted to trading on a regulated market in the European Union – i.e., unlisted – SMEs.

The following thresholds apply:

(a) An enterprise is a micro-enterprise if it does not exceed two of the following three thresholds:

- €450,000 in balance sheet total;

- €900,000 EUR net turnover; and/or

- an average of 10 employees

(b) A company is small if it does not exceed two of the following three thresholds:

- €5 million in balance sheet total;

- €10 million in net turnover; and/or

- an average of 50 employees

(c) A company is medium-sized if it does not exceed two of the following three thresholds:

- €25 million in balance sheet total;

- €50 million in net turnover; and/or

- an average of 250 employees

These companies do not fall within the scope of the Corporate Social Reporting Directive (CSRD) but are encouraged to use the VSME standard. Micro-enterprises are free to use only certain parts of this standard.

Structure of the VSME Standard

The VSME Standard offers two modules. They contain sustainability information on environmental, social, and corporate policy topics. Companies can use the Basic Module alone or supplement it with the Comprehensive Module.

- Basic Module: This module is the target approach for micro-enterprises and represents a minimum requirement for other companies.

- Comprehensive Module: This module specifies, in addition to the information in the basic module, data points that are likely to be requested by banks, investors, and corporate customers of the company.

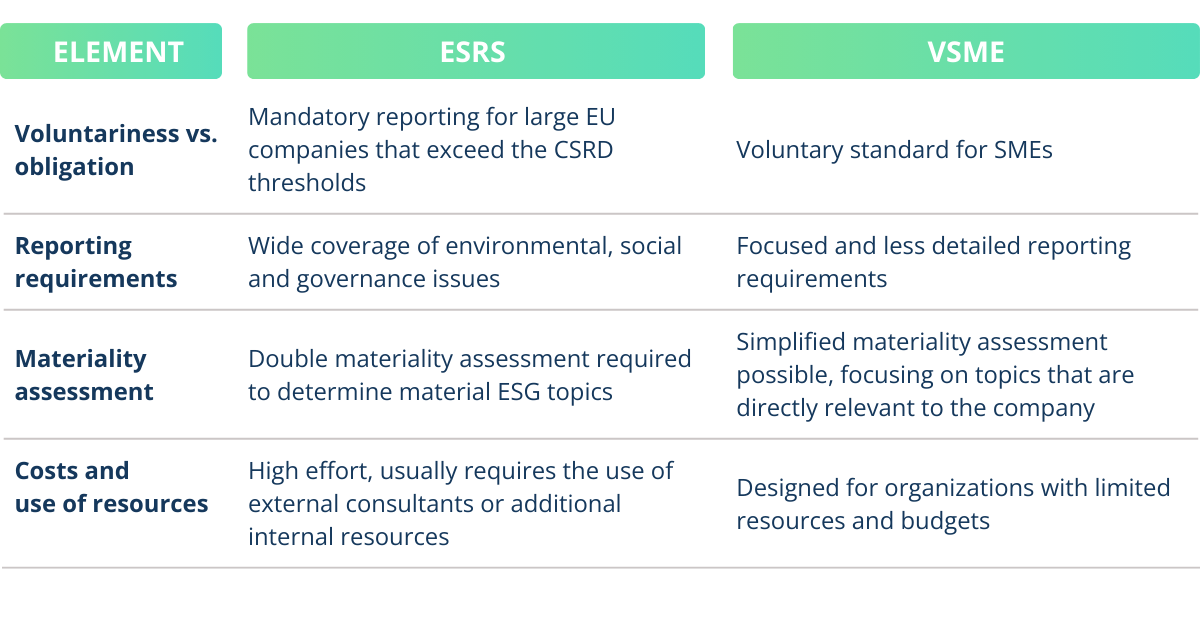

How do the ESRS and VSME standards differ?

What is the future of the VSME standard after the Omnibus proposal?

On February 26, 2025, the European Commission introduced the “Omnibus Package,” which aims to streamline sustainability reporting regulations and associated requirements. This initiative includes revisions to the Corporate Sustainability Reporting Directive (CSRD).

You can find more about the Omnibus Package here.

With the introduction of the Omnibus Initiative and the proposed small and mid-cap category, smaller companies, estimated to have 250-1,000 employees, could face new sustainability reporting requirements. Small and mid-cap companies that were not previously required to report may, in the future, also be required to provide sustainability information, but in a simplified form. This is where the VSME comes into play. The voluntary standard could provide a binding basis for these companies. However, there are no concrete statements yet about the VSME as a possibly mandatory standard; so far, it is only an idea.

According to the new Omnibus Package, the VSME standard is to be adopted by means of a delegated act. Companies that no longer fall under the CSRD reporting requirement due to the new thresholds can prepare a report that follows a voluntary reporting standard. The VSME will be the benchmark here. Companies should not be able to demand information from their suppliers, provided that they are not themselves subject to the reporting requirements that go beyond what this voluntary standard requires (so-called “value chain cap”).

Should the standard become mandatory for the new small and mid-cap category, these companies could benefit from a clear and structured but less complex solution. The VSME would enable them to efficiently capture the information required of larger, reportable companies while minimizing effort. Thus, the VSME could serve as a bridge to introduce smaller companies to the world of sustainability reporting without overwhelming them with the extensive requirements of the ESRS.

Why is the VSME standard important for SMEs even without reporting requirements?

Although SMEs are not directly required to report to the CSRD, voluntary reporting in accordance with VSME makes sense for many companies. This is because VSME standards are gaining in importance for some specific reasons:

1. Requirements from customers along the supply chain

An important factor is the trickle-down effect: large companies pass sustainability requirements down the supply chain. Specifically, this means that if a large company has to fulfill ESG reporting requirements, it will demand the corresponding data from its suppliers (often SMEs). In many cases, SMEs have not yet established systematic processes for collecting such data because they themselves are not required to report.

2. Protection against arbitrary requirements

By applying the VSME standard, SMEs can prevent major customers from overburdening them with inconsistent or excessive requests for sustainability reporting. Without clear guidelines, large companies demand individual, often very extensive sustainability information. The VSME standards could provide a structured, transparent, and recognized basis for this, protecting against “arbitrariness” from major customers.

3. Requirements of banks and ESG scores for loans

Banks and financial institutions increasingly assess companies' sustainability performance using ESG questionnaires. A good ESG score can lead to better credit terms, while a lack of ESG data can make financing more difficult. A VSME report helps SMEs respond to banks' ESG questionnaires in a targeted manner, as it provides relevant environmental, social, and governance data in a structured way.

4. Prepare for further market developments

EU directives in the area of sustainability are constantly evolving. What is voluntary today could become mandatory tomorrow, especially considering the recent Omnibus proposal (see below). SMEs that familiarize themselves with the VSME standards early will be better prepared for future regulations and can thus secure a competitive advantage.

Envoria supports you flexibly with VSME

No matter how the regulations develop, Envoria's ESG Reporting Module will keep you safe. It supports both ESRS and VSME reports and guarantees a future-proof investment.

With Envoria, you don't have to choose between ESRS and VSME – our ESG Reporting Module fully supports both standards and allows you to:

- Collect and manage all ESG data in one place

- Manage your reporting according to ESRS or VSME

- Ensure compliance no matter how regulations evolve

Want to learn more? Book a free demo.