On February 26, 2025, the European Commission presented the so-called “Omnibus Package” with the aim of simplifying the existing sustainability reporting rules and related obligations. This package includes adjustments to the thresholds, content, and timeline of the EU Taxonomy Regulation. Please note: The Omnibus proposal has not yet been finally adopted – following publication by the European Commission, it is now being examined by the relevant parliamentary committees and by the member states in the Council. During this procedure, amendments may still be made, particularly in inter-institutional negotiations (“trilogue”) if different positions exist. |

|---|

The European Union paved the way for more sustainable investments in fields including renewable energy, biodiversity, and circular economy by passing the Green Deal in 2019. The ultimate objective is to achieve climate-neutrality in Europe by 2050. Moreover, in comparison to 1990 levels, greenhouse gas emissions should be cut by 55% by 2030. Thus, the Green Deal comprises a public investment plan of 1 trillion euros over the following 10 years in order to meet these climate goals.

However, despite this huge investment, the EU depends also on the support of the private sector to achieve the Paris climate agreement. This is why the European Green Deal envisages a broad range of measures affecting various sectors of the economy and industry. The European Green Deal emphasizes the importance of sustainable finance. Sustainable finance requires the incorporation of sustainability considerations into investment and financing decision-making processes through the use of ESG (environmental, social, and governance) criteria.

As part of the European Green Deal, the EU has outlined the Sustainable Finance Framework, which is intended to help embed sustainability factors at various levels of the economy. The Sustainable Finance Framework includes the application of new EU regulations on corporate transparency. The three most important are the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD), and the Sustainable Finance Disclosure Regulation (SFDR).

Before taking a closer look at the EU Sustainable Finance Framework, let's briefly map what the EU Taxonomy, CSRD, and SFDR deal with.

The most important EU regulations on sustainability reporting

The EU Taxonomy for sustainable economic activities

As part of the European Green Deal, the EU Taxonomy Regulation sets criteria to determine if an economic activity can be considered sustainable. According to the EU Taxonomy, a sustainable economic activity has to be assigned to a defined taxonomy activity by the EU, contribute substantially to one of six defined environmental objectives, do not significantly harm any of the remaining environmental objectives, and comply with a series of minimum social safeguards. The goal of the regulation is to reorient capital flows to focus on sustainable investments and business activities including areas such as circular economy, renewable energy, and biodiversity. The reporting requirements will come into effect over a period of several years, which started in the financial year 2021.

Learn more about the EU Taxonomy regulation and its requirements in our article: What is the EU Taxonomy and which companies are required to report?

The Corporate Sustainability Reporting Directive (CSRD) for disclosure of ESG data

The Corporate Sustainability Reporting Directive (CSRD) establishes a uniform framework for the reporting of non-financial data for companies operating in the European Union. With its entry into force on January 5, 2023, the CSRD will gradually replace the Non-Financial Reporting Directive (NFRD) starting in 2024. The CSRD will significantly expand the scope of companies subject to mandatory reporting, presumably from 11,600 to 50,000 EU companies. In their report, companies must cover their key ESG areas such as environment, human rights, social responsibility, diversity, etc. One of the main innovations of the CSRD is the introduction of the concept of double materiality. Double materiality means that companies must report not only on the impact of environmental changes on their business but also on the impact of their operations on the environment (including social and governance issues).

Learn more about the CSRD and its requirements in our article All you need to know about the Corporate Sustainability Reporting Directive (CSRD).

The Sustainable Finance Disclosure Regulation (SFDR) for the financial sector

The EU Sustainable Finance Disclosure Regulation (SFDR) is a set of rules which requires financial market participants to provide information about how they deal with negative environmental and social impacts and risks of their investments. By increasing transparency, the disclosure requirements of the SFDR are intended to illustrate to investors and the public the extent to which companies or products meet sustainability benchmarks. The SFDR has two levels: product-related disclosures and entity-related disclosures. Under the SFDR, companies must disclose so-called PAI indicators (principal adverse impacts on sustainability) that establish sustainability factors for investment decisions. The EU officially introduced the SFDR in 2019, with mandatory disclosure of sustainability data since March 10, 2021.

Learn more about the SFDR and its requirements in our article Sustainable Finance Disclosure Regulation (SFDR): How it impacts your business.

Framework | EU Taxonomy | Corporate Sustainability Reporting Directive (CSRD) | Sustainable Finance Disclosure Regulation (SFDR) |

Target Group | (1) Large public-interest companies already subject to the NFRD, | (1) Large public-interest companies already subject to the NFRD, (2) all large companies that are not presently subject to the NFRD meeting certain criteria, | Financial market participants offering investment products, and financial advisers |

Disclosure requirement | Turnover, capital, and operating expenditures in the reporting year from products or activities associated with Taxonomy | Report on the basis of formal reporting standards (European Sustainability Reporting Standards, ESRS) and subject to external audit | Entity and product level disclosure on sustainability risks and principal adverse impacts |

Reporting | Starting from reporting period 2021 | Starting from reporting period 2024 | Starting from reporting period 2022 |

What is the EU Sustainable Finance Framework?

The EU Sustainable Finance Framework seeks to play a significant part in assisting the EU to achieve its climate goals and aid in the long-term recovery from the COVID pandemic. In order to meet the 2030 emissions-reduction target, the EU will need an estimated EUR 350 billion in investment annually in the field of energy systems alone over this decade. Additionally, around EUR 130 billion in investment will be required, according to the EU Commission.

Therefore, the primary goal of the sustainable finance framework is to redirect private financial flows into sustainable economic activity because the scale of investment required is significantly more than what the public sector is able to provide. Although there has been a significant increase in private interest in sustainable investment over the past few years, a robust, transparent, and unambiguous framework for sustainable finance is still needed. The EU Sustainable Finance Framework is intended to increase corporate transparency – therefore reducing the attractiveness of investment in unsustainable activities and assets and facilitating the opportunity to raise sustainable capital.

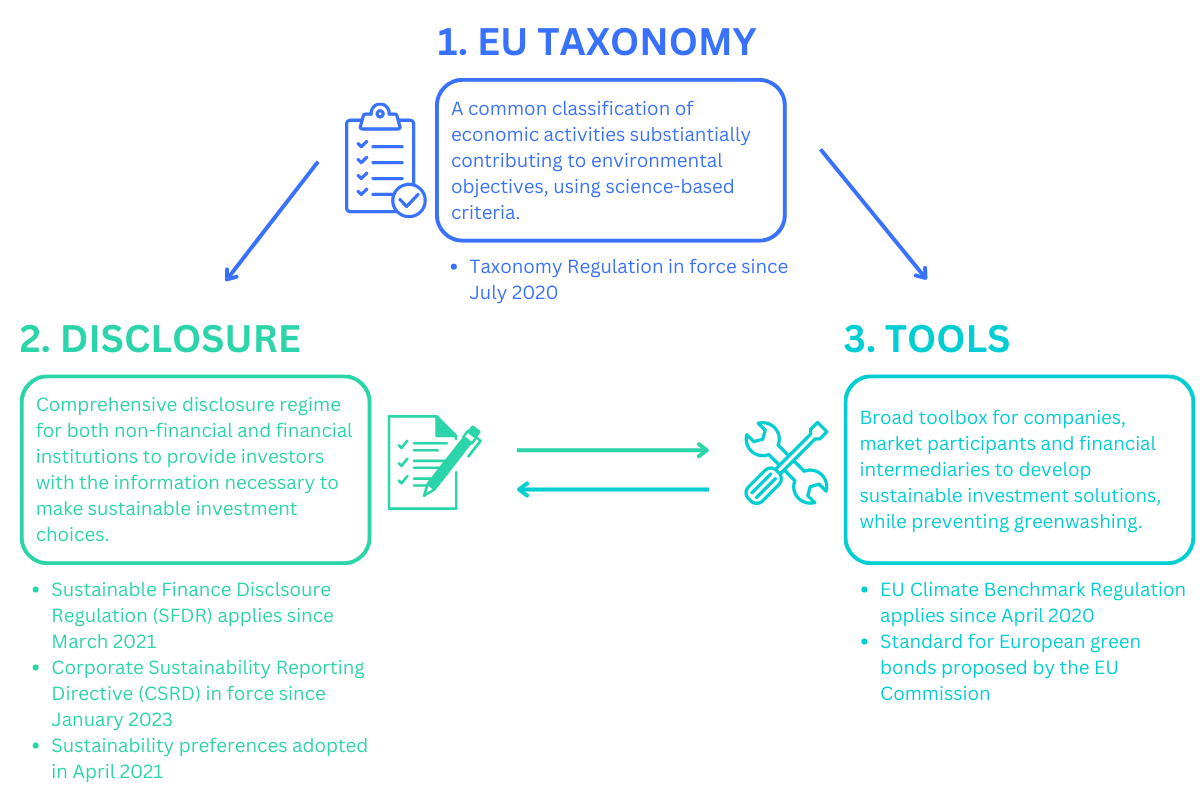

The Sustainable Finance Framework is organized into three components. These are:

The EU Taxonomy classification system for identifying sustainable economic activities

A disclosure framework for non-financial and financial companies

Investment tools including benchmarks, standards, and labels

Own illustration based on: EU Commission

{kind=link}

1. The EU Taxonomy classification system for sustainable activities

The EU Taxonomy serves as the first fundamental building block of the Sustainable Finance Framework. The EU Taxonomy provides a definition of what characteristics economic activities must possess in order to be classified as sustainable. It thus establishes a framework for a uniform understanding of sustainability for non-financial and financial organizations.

2. Disclosure requirements in non-financial statements

The second building block entails obligatory disclosure requirements for both financial and non-financial businesses, making the data that is required to choose sustainable investments available to investors. The disclosure requirements cover a company’s activities' impact on environmental and social issues. Furthermore, they include the business and financial risks a company faces due to its sustainability impact, which is also known as the double materiality approach to sustainability aspects. Mandatory disclosure requirements are defined by the CSRD for EU companies and the SFDR for financial market participants and financial advisors.

To complement these disclosure requirements, sustainability preferences must be included in financial firms’ advisory and portfolio management processes, as well as in investment and insurance advice to ensure that clients’ sustainability preferences are taken into account.

3. Tools for sustainable investment solutions

The third building block is a range of investment tools, including benchmarks, standards, and labels. These make it easier for financial market participants to align their investment strategies with the EU’s climate and environmental goals by providing greater transparency to market participants.

The EU Climate Benchmark Regulation incorporates benchmarks for specific objectives such as climate transition and adherence to the Paris Agreement. The 2021 published proposal for a European green bonds standard aims to create a standard that helps attract sustainable investments.

The relationship between the EU Taxonomy, CSDR, and SFDR

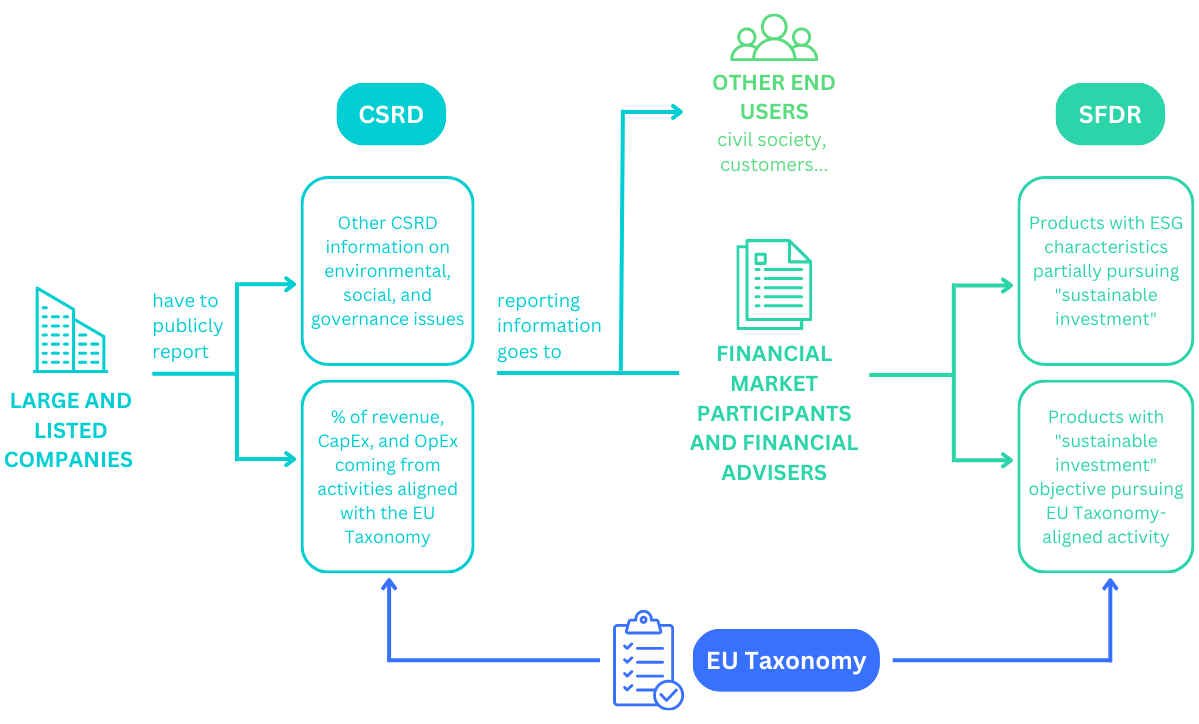

EU Taxonomy, CSRD, and SFDR are the three main EU regulatory frameworks anchored in the EU Sustainable Finance Framework. The three regulations are closely interrelated. The EU Taxonomy provides a classification system for sustainable economic activities that is applied within the CSRD and SFRD.

The CSRD requires companies to publish sustainability metrics about their economic activities. Therefore, companies affected by the CSRD must include among others the EU Taxonomy-aligned share of their turnover, capital expenditures (CapEx), and operating expenditures (OpEx) generated by their economic activities in their CSRD report. Thus, the key figures and information based on the EU Taxonomy will be integrated into the CSRD report of large companies in the future.

Financial companies affected by the SFDR must also publish taxonomy-based metrics and disclosures for ESG financial products. This applies to financial products that have the full or partial objective of making "sustainable investments". Thus, in order to comply with SFDR reporting requirements, financial companies must report the proportion of their respective financial products that are invested in taxonomy-aligned activities. This applies, for example, to information on the greenhouse gas emissions of the investments that underlie the financial products. In order to determine the required taxonomy figures, financial companies will in turn need information from the CSRD reports of the companies in which they invest. The CSRD is therefore also relevant for the SFDR, as it provides part of the information to be disclosed for the SFDR report.

In summary, the publication of the EU Taxonomy metrics is part of the reporting obligation of companies covered by the CSRD. Companies affected by the SFDR in turn need the EU Taxonomy metrics from the CSRD report of their investment objects in order to fulfill their reporting obligation. The reporting obligations of the three EU regulations are thus interlinked and overlap in terms of content.

Own illustration based on EU Commission

Prospects and challenges due to the EU Sustainable Finance Framework

With the Sustainable Finance Framework, the EU has taken an important step towards a more climate-friendly European economy. It obliges financial and non-financial companies to disclose ESG information, thus increasing transparency with regard to corporate sustainability. This is intended to achieve the goal of reorienting capital flows toward more sustainable investments.

The three most important regulations that compose the Sustainable Finance Framework – the EU Taxonomy, the Corporate Sustainability Disclosure Regulation, and the Sustainable Finance Disclosure Regulation – are closely interlinked. While the EU Taxonomy provides the classification framework for sustainable activities, the CSRD regulates sustainability reporting and the SFDR defines the disclosure requirements for selling financial products. These regulations affect all major players along entire investment value chains, from companies that demand capital to investors that provide funding to those companies, and everyone in between.

The new EU regulations on sustainability reporting are accompanied by a large number of challenges. This applies in particular to those companies that have not yet been engaged in sustainability reporting. But also for companies that already report on ESG topics, the requirements regarding data quality and scope are becoming more stringent.

Companies should therefore deal with the consequences of the new disclosure requirements under the regulations of the EU Sustainable Finance Framework at an early stage. Timely preparation is essential to ensure smooth implementation. The establishment of the necessary internal structures for data collection and reporting on sustainability issues as well as the successful implementation of the EU regulations will be among the key tasks for the affected companies in the coming years.